Industrial Outdoor Storage Surges Into Stardom

March 18, 2026

What might appear to casual observers as little more than vacant lots is quickly becoming one of the most sought-after segments in industrial real estate.

According to a recent fourth-quarter 2025 report from CBRE, industrial outdoor storage (IOS) is gaining momentum and delivering standout performance across the sector.

The report highlights IOS as an increasingly competitive niche within industrial and logistics real estate. These properties cater to industries such as construction, utilities, trucking, equipment, and government operations. Their appeal lies in their strategic locations near job sites and transportation corridors, combined with minimal infrastructure requirements—factors that help keep costs low and cash flow steady.

CBRE’s analysis focused on a specific subset of properties: those with less than 20% building coverage, no more than 50,000 square feet of structures, and total site sizes under 40 acres. Only single-tenant, net-leased assets were included.

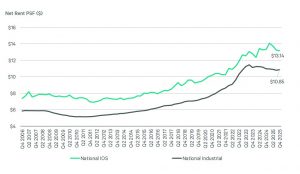

Within these parameters, IOS significantly outperformed traditional industrial properties. In Q4 2025, IOS rents averaged $13.14 per square foot, compared to $10.85 for conventional industrial space—a 17.9% premium that has continued to grow year over year.

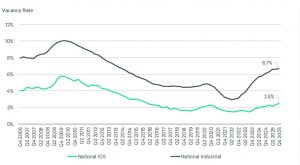

Limited supply is a key driver of this performance. IOS vacancy stood at just 2.5% in the fourth quarter, far below the 6.7% rate for traditional industrial assets. Development remains difficult due to restrictive zoning regulations and increasing community resistance, reinforcing tight supply, strong tenant retention, and sustained pricing power.

Secondary markets positioned between major logistics hubs are seeing particularly strong rent premiums. Cities like Kansas City, Indianapolis, Charlotte, and Cincinnati stand out, while emerging hotspots include Kansas City, Los Angeles, Savannah, Columbus, and El Paso.

CBRE’s Vice President and Global Head of Industrial Research for the Americas, James Breeze, points to several structural constraints limiting IOS expansion. These sites are typically located in dense urban areas near key logistics infrastructure—airports, rail lines, highways, and ports—where available land is scarce.

At the same time, demand continues to rise, fueled by growth in manufacturing, domestic energy production, and infrastructure investment. For many users, storing materials outdoors is far more cost-effective than leasing warehouse space, especially when proximity to transportation networks reduces overall logistics costs.

Net leases are also common in the IOS sector, largely due to the limited infrastructure involved. Tenants typically take responsibility for expenses such as taxes, insurance, and maintenance of essential features like paving, fencing, lighting, and drainage—giving them greater control over operating costs.

With few viable alternatives—aside from leasing lower-grade warehouses with yard space—IOS is becoming one of the most constrained and competitive asset classes in industrial real estate today.

Source: Commercial Property Executive